You are currently browsing the tag archive for the ‘andhra pradesh’ tag.

Last week at the International Studies Association Conference in Toronto, Marie Langevin (Ottawa) and I hosted a panel bringing together Northern and Southern perspectives on what may be termed poverty finance*. These perspectives surprisingly only rarely speak to each other, and our panel demonstrated how important and fruitful such a conversation is. Phil Cerny chaired the panel “Fringe Finance and Financial Inclusion”, and Rob Aitken (Alberta) – one of the few exceptional researchers whose work spans both the worlds of Northern and Southern poverty finance – acted as discussant of the papers.

The papers…

It’s good to see microfinance researchers seriously studying alternatives to microloans or other microfinancial services. Very poor people need assets and a helping hand more than a loan, so why not hand out a cow or some other income-generating assets, offer training, and provide basic healthcare? That’s what an 18-month “Ultra-Poor Programme” run by SKS Microfinance in India did. But the randomised impact evaluation performed by Jonathan Morduch of New York University, Shamika Ravi of the Indian School of Business and Jonathan Bauchet of Purdue University on this programme turned up a “null” result, similar to those of randomised studies of microfinance.

Perhaps it is surprising to see SKS Microfinance (India’s largest microlender before 2010, and now perhaps most notorious microlender) giving non-repayable one-off kickstarts to ultra-poor households. But the intention of the programme was not purely altruistic; it was to “graduate” households into microfinance, by giving them assets to start a business.

In the programme in Andhra Pradesh evaluated by Morduch/Ravi/Bauchet, people who got a free asset and training to become microentrepreneurs were found to be no better off later than those who didn’t. They also didn’t manage to reduce their debts or increase their savings any more than others. Why? The authors believe it is

explained in large part by substitution with other economic activities. […] During the study period, wages in agricultural labor were rising steadily in the region, so that households in the control group were able to improve their economic conditions in parallel with households in the treatment group. (35)

The opportunities outside the self-employment programme offered similarly improving incomes as the opportunities offered by the programme itself. To what conclusion should this lead us about the concept of entrepreneurial self-lift out of poverty? Overall, the take-home message from the authors is eminently logical:

One of the things that make blogs particularly interesting are series. The “series” series recommends series at related blogs.

When Daniel Rozas warns, I listen. Rozas forecasted the crisis of microfinance which broke out in India in late 2010, warning as early as November 2009 that Andhra Pradesh was the most saturated microfinance market in the world alongside Bangladesh, and mass defaults could begin any time.

2009:

I can’t predict whether the microfinance bubble I believe exists and continues to grow in Andhra Pradesh and other south Indian states will deflate quietly or burst spectacularly. […] In their pursuit of growth, many MFIs have continued to add large numbers of new customers in Andhra Pradesh and other highly saturated regions – I believe that is irresponsible. […] The spark that sets off a large-scale delinquency crisis can be anything and could come at any time – a rapid drop in economic growth, a populist political movement, a religious decree, or a collections effort gone bad. One can’t control the spark, but one can control how much fuel that spark can ignite.

Since this February, Rozas has been outlining the scenario of a possible further repayment crisis in a series of posts (links to parts 2 & 3) on the Financial Access Initiative Blog. He says self-regulatory efforts over the past years have been important, but perhaps not enough to stem lending excesses in certain countries (I would agree). Looking at indebtedness and lending at the sub-national level, Rozas reveals a fairly alarming picture in the Mexican state Chiapas, which shows similar patterns to Andhra Pradesh in 2009.

But it is Rozas’ attunement to the political economy of microlending which sets him apart from most sector consultants. Read the rest of this entry »

The Andhra Pradesh crisis has been something of a turning point in public assessment of microfinance, with a suicide wave caused by widespread overindebtedness badly tarnishing the sector’s image in India as well as abroad. Some Indian politicians are now beginning to identify the idea of alleviating poverty with microfinance as “crap“.

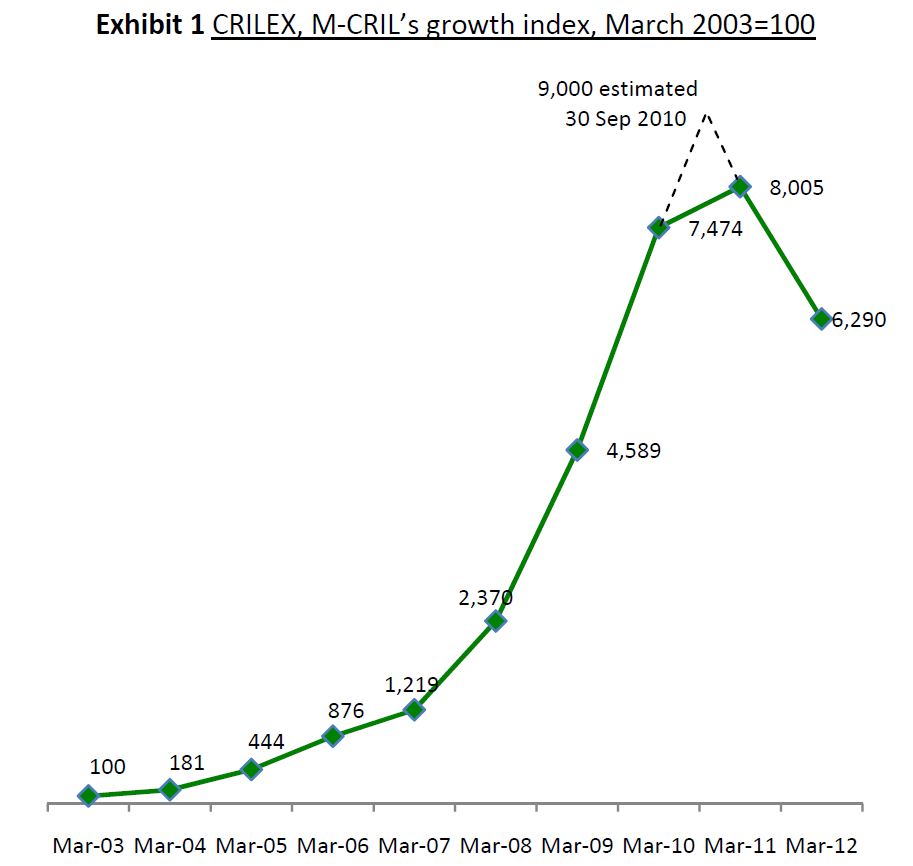

Source: M‐CRIL Microfinance Review 2012 (vii)

Microfinance in India remains in protracted decline since 2010 (see graph), although talk of “green shoots” and catharsis after “near-death experience” has been around for some time. The industry’s stance for the past two years has been to deny responsibility for any wrongdoings, downplay its role in precipitating the dozens of suicides, and claim that the AP government’s October 2010 legislation was a surprising and unjust crackdown on healthy practices. I have claimed otherwise.

Yet, fairly surprisingly, my new paper investigating the causes of the crisis, and a recent interview with SKS Microfinance senior managers come to some similar conclusions about the causes. In particular, both versions see the unregulated hyper-competitive market as a significant cause of the tragedy which led to microfinanciers’ troubles. How can this be?

Ramesh S. Arunachalam, 2011: The Journey of Indian Micro-Finance: Lessons for the Future. Chennai: Aapti Publications.

Ramesh S. Arunachalam, 2011: The Journey of Indian Micro-Finance: Lessons for the Future. Chennai: Aapti Publications.

The microfinance crisis in India which broke out in fall 2010, first imperiling numerous borrowers and then an entire industry, is the most fundamental event in the world of microfinance since the Nobel Peace Prize in 2006. In hindsight, it may even turn out to be the defining moment of microfinance history – never before has the dark side of microfinance, and the vulnerability of the industry, been so brutally exposed to a global audience.

Naturally, these events have attracted a host of opinions and analyses ranging from simply blaming the Andhra government for bringing down a healthy microfinance industry, to accusing microfinance of having become worse than loan sharks. And yet, so far, we understand very little of why India’s vast microfinance sector went so far astray. Thankfully, people like Ramesh S. Arunachalam are out to change this.

Arunachalam has earned the respect of many a reader (me too) with his candid and incredibly well-researched blogging on the Indian microfinance sector. He posts prolifically, but despite (or perhaps because of) his over 20 years of work experience in development and rural finance, he has otherwise kept a low profile. He is not an outspoken critic.

Now Ramesh Arunachalam has applied his sharp analytical approach and evident knack for writing to publishing the first book about the Indian microfinance crisis. The result is a meticulous, evidence-based piece of research which brings clarity into what so far has mostly been an interest-driven and polemical battle of explanations.

In some ways what Arunachalam has produced is, in fact, more than a book; it is a dossier of evidence and analysis of how the Indian microfinance sector functions at the deepest levels, and where its errors lie. It is a biography of an industry in identity crisis, and also a handbook on how Indian microfinance might (perhaps) still be saved. Above all, as the book’s (wonderfully illustrative) cover implies, it is a search for the Faustian, troubled soul of Indian microfinance. Read the rest of this entry »

Microfinance in India is still where it was months ago – in a stalemate with the government. The crisis of microcredit in the southern Indian state of Andhra Pradesh which began last October with a rash of client suicides – we were the first to blog about this, and followed its development throughout – climaxed in a standoff in late October between the state legislature and microfinance institutions (MFIs). Mud was thrown by both sides in an intense blame-game, while actually the crisis had systemic causes rooted in weak legislation and a hyper-competitive market.

Neither side has found a way to break out. But the stalemate is becoming unstable. It is increasingly clear to MFIs and their funders that most loans in Andhra Pradesh will not be recoverable, since trust in the MFIs’ promise of being “here to stay” is dwindling, and the new legislation has rendered erstwhile coercive recovery practices impossible. On the other hand, the Andhra government cannot step down from its legislature issued under the promise of protecting the poor without losing face, and the Indian federal government has chosen to largely ignore the issue.

The Economic Times from Mumbai recently provided a thorough update on what happened in the past few months, which I’m quoting here. The growing problem is that the MFIs in Andhra Pradesh will need new capital soon in order to replace the loans they have written off, or will soon be forced to write off. Read the rest of this entry »

The reactions to Tom Heinemann‘s controversial documentary “The Micro Debt” have mostly been strong. The film sheds light onto a number of questions, first and foremost the risk microcredit borrowers face of becoming trapped in debt. However, public debate has so far focused on two rather marginal parts of the film: a more-or-less resolved dispute over aid money (cf. “GrameenLeaks”), and a dispute about a house supposedly promised in the village of Jobra. It is worth investigating why so much publicity has been given to these two issues, and so little to the film’s main message: that microfinance can cause debt traps.

While the charges of financial malpractice in the Grameen conglomerate have now been largely cleared up, Muhammad Yunus still remains a target of negative attention from the Bangladeshi government. He is now apparently no longer Grameen Bank’s director. But Yunus’ personality and job status should have nothing to do with an impartial assessment of the virtues of microfinance. What becomes clear from the recent debate is how symbols are mobilised (and abused) in legitimising as well as challenging microfinance. However, this distracts from more substantial questions about what microfinance does or doesn’t, can or can’t, achieve.

Let us take a look at “The Micro Debt” and the reactions to it, and also take a look at another, less-known documentary with less impact but perhaps a better focus on substance: “Easy Money”. Both films make the allegation that microfinance can be exploitative and can cause more problems than it solves. But the reason why “The Micro Debt” has been perceived as so inflammatory, while “Easy Money” apparently has hardly been discussed at all, is that “The Micro Debt” attacks microfinance’s symbolic self-representations of success and integrity. Read the rest of this entry »

In this interview, Professor Malcolm Harper analyses some of the underlying causes and consequences of the microfinance crisis in Andhra Pradesh. Professor Harper is chairman of the microfinance rating agency M-CRIL and editor of the volume “What’s wrong with Microfinance?”. He has been Professor of Business Development at Cranfield Business School, and as the former chairman of BASIX, significantly pioneered microfinance in India.

Professor Harper, you recently returned from India. How bad is the situation for the microfinance sector there?

I was in Delhi at a very large meeting of microfinance people, where of course Andhra Pradesh was being talked about a lot. I then spent some time in Orissa, in a village three kilometres from the Andhra Pradesh border. I called in on the local office – which previously I didn’t even know existed – of BASIX. And the local staff said there had been no trace of any repayment difficulties, even though the Andhra Pradesh border was so close by. This surprised me, and even they were rather surprised. Repayments were at the normal high level.

But I was running a course nearby and my students were interviewing various traders in the local market, and a few of them mentioned that one or two of the microfinance institutions, from which they had taken loans, had stopped making disbursements. And that of course has the seeds of trouble, because one reason why people repay is because they’re going to get another loan.

So it seems that the MFIs are having trouble refinancing themselves now, raising capital for their lending activities.

That’s inevitable, I think, because when the banks are beginning to wonder about the quality of their loans to the MFIs, they’re not about to release further loans. And that, of course, contributes to the problem, because – as I said – people repay mainly because they’re going to get another loan. Read the rest of this entry »

In the past few weeks, I’ve been silent here about the microfinance crisis events in India. But why not let others do the talking? This blog published (what I think was) the first analysis of the A.P. events right after the crackdown ordinance; following up with a two-piece search for the underlying causes (1, 2). Most of the causes I speculated about at the time are pretty much turning out to be true:

- interest rates were far too high and have been rushed down

- the sector was under-, or practically un-, regulated (especially, if Kaushik Basu says so)

- the borrowers were/are overindebted (far more than the MFIs were aware of, I assume)

- and the profit motive created perverse incentives for MFIs.

One prediction I won’t make, though, is whether microfinance in India will pull through. That depends on politics in Delhi (bailout or not?) as much as it does on the adaptiveness (not the resilience, which means “no change”) of the sector. But I wouldn’t bet my money on an MFI in India at the moment, given the pessimism of Vijay Mahajan (“If this situation continues, there will be no microfinance sector in 2011.”) or the SKS’ shareholders (shares down by 52 percent).

The real surprise story of the week, however, were WikiLeaks’ diplo-inslults.

Or really, were they? Only the Americans are really making a big deal out of the leaked diplomatic cables. If anything, the now-public secret assesments of sundry politicians should provide a few good-natured jokes at upcoming international summits. Would-be Israel-nukester Ahmadinejad will hardly be insulted by being compared with “Hitler”, and German Chancellor Angela Merkel and Foreign Minister Guido Westerwelle already had their share of laughs about “their” leaks.

… that lower interest rates were possible all along!

India’s embattled microfinance industry has agreed to cap interest rates on its loans in southern Andhra Pradesh state at 24 per cent, as it seeks to counter an intense political backlash against the sector. …

Previously, the industry insisted its high interest rates were needed to cover the cost of outreach to so many small borrowers. However, it has decided to cap the rates in a bid to reduce antagonism from Indian policymakers, who are increasingly uncomfortable with the large profits and personal fortunes being amassed in an industry ostensibly dedicated to alleviating poverty. (ft.com)

And in The Hindu:

“We’ve made several concessions because we’re under duress and not because we want to. It is against our model, but we want the sector to survive. Mr Gopalan completely understands our situation, but he has not let us off the hook,” said Mr Vijay Mahajan, President, MFIN.