You are currently browsing the category archive for the ‘Andhra Pradesh Microfinance Crisis’ category.

The Andhra Pradesh crisis has been something of a turning point in public assessment of microfinance, with a suicide wave caused by widespread overindebtedness badly tarnishing the sector’s image in India as well as abroad. Some Indian politicians are now beginning to identify the idea of alleviating poverty with microfinance as “crap“.

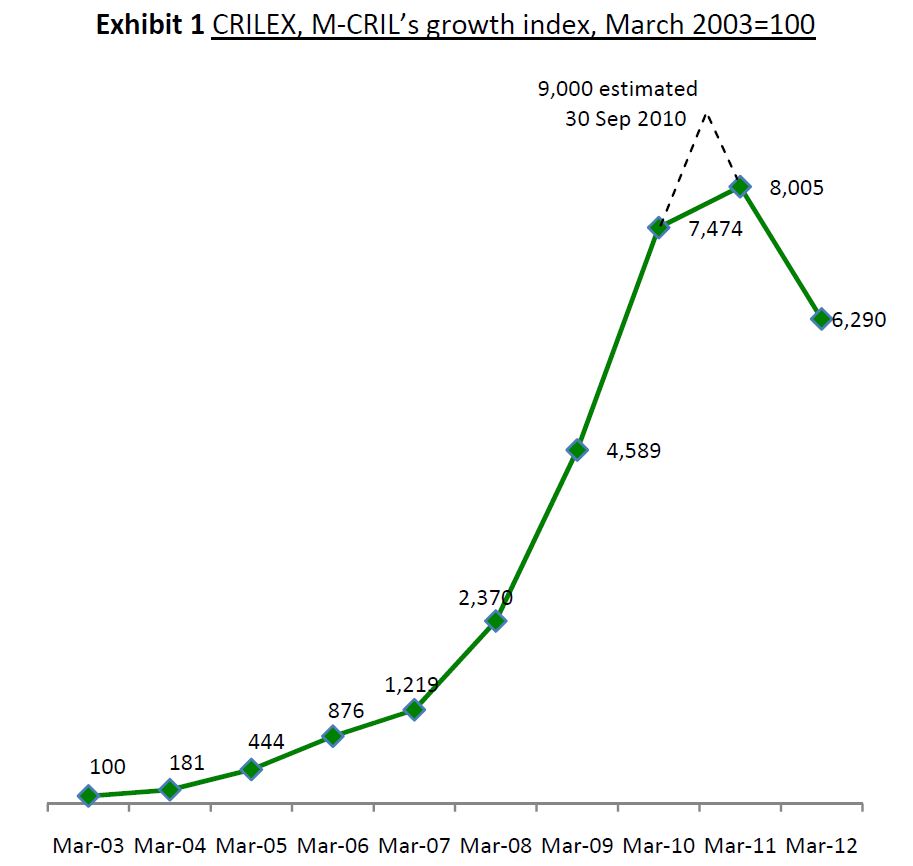

Source: M‐CRIL Microfinance Review 2012 (vii)

Microfinance in India remains in protracted decline since 2010 (see graph), although talk of “green shoots” and catharsis after “near-death experience” has been around for some time. The industry’s stance for the past two years has been to deny responsibility for any wrongdoings, downplay its role in precipitating the dozens of suicides, and claim that the AP government’s October 2010 legislation was a surprising and unjust crackdown on healthy practices. I have claimed otherwise.

Yet, fairly surprisingly, my new paper investigating the causes of the crisis, and a recent interview with SKS Microfinance senior managers come to some similar conclusions about the causes. In particular, both versions see the unregulated hyper-competitive market as a significant cause of the tragedy which led to microfinanciers’ troubles. How can this be?

Ramesh S. Arunachalam, 2011: The Journey of Indian Micro-Finance: Lessons for the Future. Chennai: Aapti Publications.

Ramesh S. Arunachalam, 2011: The Journey of Indian Micro-Finance: Lessons for the Future. Chennai: Aapti Publications.

The microfinance crisis in India which broke out in fall 2010, first imperiling numerous borrowers and then an entire industry, is the most fundamental event in the world of microfinance since the Nobel Peace Prize in 2006. In hindsight, it may even turn out to be the defining moment of microfinance history – never before has the dark side of microfinance, and the vulnerability of the industry, been so brutally exposed to a global audience.

Naturally, these events have attracted a host of opinions and analyses ranging from simply blaming the Andhra government for bringing down a healthy microfinance industry, to accusing microfinance of having become worse than loan sharks. And yet, so far, we understand very little of why India’s vast microfinance sector went so far astray. Thankfully, people like Ramesh S. Arunachalam are out to change this.

Arunachalam has earned the respect of many a reader (me too) with his candid and incredibly well-researched blogging on the Indian microfinance sector. He posts prolifically, but despite (or perhaps because of) his over 20 years of work experience in development and rural finance, he has otherwise kept a low profile. He is not an outspoken critic.

Now Ramesh Arunachalam has applied his sharp analytical approach and evident knack for writing to publishing the first book about the Indian microfinance crisis. The result is a meticulous, evidence-based piece of research which brings clarity into what so far has mostly been an interest-driven and polemical battle of explanations.

In some ways what Arunachalam has produced is, in fact, more than a book; it is a dossier of evidence and analysis of how the Indian microfinance sector functions at the deepest levels, and where its errors lie. It is a biography of an industry in identity crisis, and also a handbook on how Indian microfinance might (perhaps) still be saved. Above all, as the book’s (wonderfully illustrative) cover implies, it is a search for the Faustian, troubled soul of Indian microfinance. Read the rest of this entry »

Microfinance in India is still where it was months ago – in a stalemate with the government. The crisis of microcredit in the southern Indian state of Andhra Pradesh which began last October with a rash of client suicides – we were the first to blog about this, and followed its development throughout – climaxed in a standoff in late October between the state legislature and microfinance institutions (MFIs). Mud was thrown by both sides in an intense blame-game, while actually the crisis had systemic causes rooted in weak legislation and a hyper-competitive market.

Neither side has found a way to break out. But the stalemate is becoming unstable. It is increasingly clear to MFIs and their funders that most loans in Andhra Pradesh will not be recoverable, since trust in the MFIs’ promise of being “here to stay” is dwindling, and the new legislation has rendered erstwhile coercive recovery practices impossible. On the other hand, the Andhra government cannot step down from its legislature issued under the promise of protecting the poor without losing face, and the Indian federal government has chosen to largely ignore the issue.

The Economic Times from Mumbai recently provided a thorough update on what happened in the past few months, which I’m quoting here. The growing problem is that the MFIs in Andhra Pradesh will need new capital soon in order to replace the loans they have written off, or will soon be forced to write off. Read the rest of this entry »

In this interview, Professor Malcolm Harper analyses some of the underlying causes and consequences of the microfinance crisis in Andhra Pradesh. Professor Harper is chairman of the microfinance rating agency M-CRIL and editor of the volume “What’s wrong with Microfinance?”. He has been Professor of Business Development at Cranfield Business School, and as the former chairman of BASIX, significantly pioneered microfinance in India.

Professor Harper, you recently returned from India. How bad is the situation for the microfinance sector there?

I was in Delhi at a very large meeting of microfinance people, where of course Andhra Pradesh was being talked about a lot. I then spent some time in Orissa, in a village three kilometres from the Andhra Pradesh border. I called in on the local office – which previously I didn’t even know existed – of BASIX. And the local staff said there had been no trace of any repayment difficulties, even though the Andhra Pradesh border was so close by. This surprised me, and even they were rather surprised. Repayments were at the normal high level.

But I was running a course nearby and my students were interviewing various traders in the local market, and a few of them mentioned that one or two of the microfinance institutions, from which they had taken loans, had stopped making disbursements. And that of course has the seeds of trouble, because one reason why people repay is because they’re going to get another loan.

So it seems that the MFIs are having trouble refinancing themselves now, raising capital for their lending activities.

That’s inevitable, I think, because when the banks are beginning to wonder about the quality of their loans to the MFIs, they’re not about to release further loans. And that, of course, contributes to the problem, because – as I said – people repay mainly because they’re going to get another loan. Read the rest of this entry »

In the past few weeks, I’ve been silent here about the microfinance crisis events in India. But why not let others do the talking? This blog published (what I think was) the first analysis of the A.P. events right after the crackdown ordinance; following up with a two-piece search for the underlying causes (1, 2). Most of the causes I speculated about at the time are pretty much turning out to be true:

- interest rates were far too high and have been rushed down

- the sector was under-, or practically un-, regulated (especially, if Kaushik Basu says so)

- the borrowers were/are overindebted (far more than the MFIs were aware of, I assume)

- and the profit motive created perverse incentives for MFIs.

One prediction I won’t make, though, is whether microfinance in India will pull through. That depends on politics in Delhi (bailout or not?) as much as it does on the adaptiveness (not the resilience, which means “no change”) of the sector. But I wouldn’t bet my money on an MFI in India at the moment, given the pessimism of Vijay Mahajan (“If this situation continues, there will be no microfinance sector in 2011.”) or the SKS’ shareholders (shares down by 52 percent).

The real surprise story of the week, however, were WikiLeaks’ diplo-inslults.

Or really, were they? Only the Americans are really making a big deal out of the leaked diplomatic cables. If anything, the now-public secret assesments of sundry politicians should provide a few good-natured jokes at upcoming international summits. Would-be Israel-nukester Ahmadinejad will hardly be insulted by being compared with “Hitler”, and German Chancellor Angela Merkel and Foreign Minister Guido Westerwelle already had their share of laughs about “their” leaks.

… that lower interest rates were possible all along!

India’s embattled microfinance industry has agreed to cap interest rates on its loans in southern Andhra Pradesh state at 24 per cent, as it seeks to counter an intense political backlash against the sector. …

Previously, the industry insisted its high interest rates were needed to cover the cost of outreach to so many small borrowers. However, it has decided to cap the rates in a bid to reduce antagonism from Indian policymakers, who are increasingly uncomfortable with the large profits and personal fortunes being amassed in an industry ostensibly dedicated to alleviating poverty. (ft.com)

And in The Hindu:

“We’ve made several concessions because we’re under duress and not because we want to. It is against our model, but we want the sector to survive. Mr Gopalan completely understands our situation, but he has not let us off the hook,” said Mr Vijay Mahajan, President, MFIN.

As India celebrates Diwali this week, the debate about how to deal with microfinance has calmed a bit. But since I wrote up my analysis of the root causes Andhra Pradesh showdown (part 1, part 2), the news has taken few further twists. Here’s an update:

- Vijay Mahajan, Chairman of BASIX and speaker for the MFIN industry organisation, stated on TV: “Alot of the reasons for invoking the ordinance were the creation of the microfinance sector itself. There has been a certain degree of wrongdoing by our sector. And as the president [of MFIN] I am the first one to accept it, I want to do it on record.”

- The interest rate disclosure requirement under the new microfinance ordinance in AP has uncovered interest rates far higher than previously reported – up to 60.5 percent. I wish I was surprised; but MFIs usually neglect to factor compulsory savings, fees, etc., into their publicly quoted rates.

- The AP government has published the complete list of complaints of malpractice and suicide launched against the MFIs – see it here.

- A massive borrower database in AP will go on-line in January, in an effort to clear up the mess.

Meanwhile, India’s vibrant media and civil society have been grappling with the issue, as are some American media. The rest of this post is a digest of the most provocative, insightful and intelligent commentary I’ve seen on the subject.

This is the second half of my search for the causes of the microfinance crisis and suicide tragedy in Andhra Pradesh. In my last posting, I outlined the macro causes as I saw them. I found evidence that MFIs were charging borrowers interest rates over and above what they actually could have charged them. I also found that the government failed to regulate despite an evident lack of self-regulation; that is, until Andhra Pradesh clamped down two weeks ago. In this posting I search for micro-level causes.

Since my last post, SKS on Saturday posted profits up by 116 percent y-o-y (read: more than doubled), and also apparently held a secret board meeting over the weekend. You don’t need to be a Marxist to find a steep rise in profits disturbing for a bank which lost at least 17 of its clients to debt-driven suicide in the same quarter. Yet the crisis in AP is far bigger than SKS, and the five biggest MFIs’ have realised this and collectively announced last Friday to restructure distressed loans. Finally. It took nearly two months of suicides, a heavy-handed regulatory clampdown and a media backlash to drive enough sense into the MFIs. The women’s Self-Help-Group movement is also pushing for better regulation. How did we get here in the first place?

The poor are prone to debt traps

The media have caught onto some of the macro issues, but here I will identifiy drivers for the heavy debt burdens and suicides which operate at the micro level. We must be aware that suicide in India is already shockingly common among farmers. But many, if not most victims in AP were small traders, not subsistence farmers, so we’re dealing with a new phenomenon here.

It is no surprise that highly-indebted microfinance borrowers can be driven into debt spirals towards MFIs under conditions of heavy marketing, misinformation, social pressure to join self-help groups, and the vagaries of economic life at the bottom of the social order. If one thing goes wrong (an illness, a crop loss), an apparently sensibly invested loan suddenly turns into an insurmountable debt burden (see these media reports for illustrations of microfinance-funded debt traps). In reality, “India Shining” is home to some of the poorest people in the world. As we saw last week, some microfinanciers are apparently out of touch with this reality. Atul Takle of SKS went on the record telling the Associated Press, “I personally don’t think a person would take her life for 225 rupees ($5.08) a week.” But four out of five people in India live on less than 20 Rupees a day (2007; latest figure I could find).

This (self-drafted, non-exhaustive) list outlines individual causes for the poor taking on unsustainable debt. It shows that there are mulitple reasons for the poor falling into microfinance debt traps, and that most are outside of their control. Read the rest of this entry »

Maybe it’s too early to seek real explanations for the microfinance tragedy in AP. The dust hasn’t settled yet, but I’m struggling to come to grips with the big “why?”. (For a summary of events until Tuesday, see here.) My usual blog sources of all colours for all things development are silent, so far. But the Indian media are buzzing with coverage and an occasional piece of analysis. From what I can tell from these reports, the crisis was caused by a failure to regulate and a set of ultra-perverse incentives for microfinanciers and their employees.

What happened? In the past 6 weeks or so, some 30 to 60 microcredit borrowers in Andhra Pradesh (according to different sources) committed suicide over their loans. Individual stories had surfaced increasingly throughout early and mid-October about borrowers suffering under heavy debt burdens and massive pressure from agents; with measures apparently even including child abduction as punishment for loan default and agents urging borrowers to take their lives to reap credit life insurance. Protests ensued, and last week, the AP government issued an ordinance imposing rules of conduct and compulsory registration on MFIs (microfinance institutions). A consortium of MFIs (MFIN) claimed this had halted their business completely, and this week the MFIs submitted a petition at the AP High Court asking to quash the government’s ordinance.

This Indian news video concisely tells the horrific story.

The High Court today officially permitted MFIs to continue their business activities, while upholding the terms of the ordinance that MFIs may not engage in coercive practices and must proceed with registration. Meanwhile, employees of SKS Microfinance and Spandana have been arrested for harassing borrowers. SKS shares have dropped by over one fifth, indicating that investors are worried about profitability (rightly so). An Indian apex organisation has proposed for all its members to cut interest rates – more about that below. Read the rest of this entry »

This is more shocking news from Andhra Pradesh. Obligatory life insurance sold with microfinance loans may be incentivising overindebted borrowers to commit suicide. Worse yet, it appears that loan officers have been pushing debtors to commit suicide as a way out of debt.

Here’s the gist of a Times of India article by Jinka Nagaraju published earler today:

A government study has found that some MFI agents themselves are encouraging the debtors to commit suicide so that their loans are repaid. This happens because the borrowers are covered by insurance.

Till now, there have been at least 45 suicides reported in the state in the last one-and-a-half months allegedly due to the coercive practices employed by the MFIs in recovering the loans. …